4 Questions To Investigate at COP26

The UN Climate Conference (COP26)

In just under a week’s time, the city of Glasgow in Scotland will sponge up the feet, eyes and ears of participants and interest groups as the 26th Congress Parties (COP26) gets underway. From the week of the 31st of October to the 12th of November 2021 we will see Diplomats, Scientists, NGOs, Civil Societies, Academics and more engage in numerous discussions regarding the world’s future and policy thereof. This will be with respect to the aspects surrounding the climate, environment and subsequent actions required by society as whole to respond to the threat believed to be on the horizon regarding runaway greenhouse effects in tandem with potential socioeconomic issues therein.

Though prior editions of the congress have carried notable importance, it is arguable that this particular edition feels more important than previous ones. This is probably related to the zeitgeist surrounding the discussion of climate change as well as it’s confluence with modern narrative setting platforms and interconnectedness afforded by technologies such as social media and 24-hour within-palm-reach news cycles. We also cannot ignore the collective trauma that has been Covid 19 which one can argue has exacerbated the sense of priority on the global discourse of issues non-discriminatorily affecting human life on the planet from environment to health to the more structural issues like the sort of political and economic systems mankind has iteratively adopted over the centuries based on the prevailing circumstances of the time.

The aim of this inquiry-form piece is to highlight the 4 areas piquing my personal interest that I will therefore be looking out for, explicitly stated, inferred or otherwise as to the potential policy directions in store. This is therefore not exhaustive given the somewhat anecdotal nature of questions. However, I believe it forms a basis around which many elements will relate to or spawn from and are in turn the foundations of what makes the overall universe surrounding the discussion complex and in need of genuine and sincere multilateral engagement.

1) What is the position and/or action towards a Just/Fair Energy Transition especially for low industrial base economies?

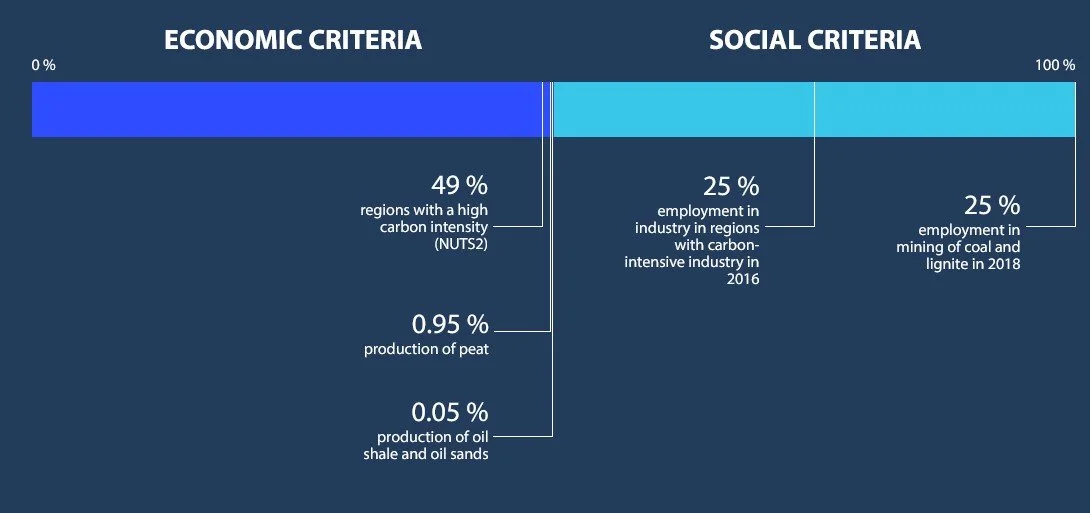

The term Just Energy Transition in the context of the modern energy discussion has its origins in Trade Union/Worker’s movements (mainly in Europe) advocating for a switch that does not disenfranchise workers in industries that the transition will render defunct - particularly in the fossil fuel space. A question that subsequently comes with this is whether the transition is a space where jobs created will offset those displaced which is a question that does not only concern the energy industry but applies to the broader trend of reduced jobs in industries technology is mechanizing and digitizing. Therefore we can expect the transition to create a new paradigm of jobs but the way to evaluate the net gain probably requires a view of overall productivity gains vs headcount gains and potentially more importantly, how the productivity output is equitably distributed. In the EU, one of the approaches being taken is to have a Just Transition Fund (JTF) currently totaling €40bn which is meant to “support regions relying on fossil fuels and high-emission industries in their green transition” e.g. Poland. The JTF allocation criteria is structured as below and offers a potential example though we know the reality that not every region would have the sort of funds available to set aside to enact something similar hence a question on how that would happen in such places.

There has also been an evolution by whichthe term Just Transition can also extend its reference to the overall socioeconomic discussions around so-called developing nations who are typically industrializing from low bases therefore coming from a low carbon emissions contribution positions and need energy sources commensurate to their aims of raising citizens quality of life and alleviating poverty. Commensurate here implying energy sources that are practically, technologically and economically viable for the scale of growth required for these human life standard advancements within at least a decade.

This discussion acts as a sprouting point for further discussion around matters such as the drying up of funding for new coal projects. Indeed, as mentioned in the article here on Take Aways from the FT Energy Transition Strategies summit, coal is the most vulnerable of the fossil fuels to this shift for reasons associated with it’s emissions contribution footprint but also it’s perceived substitutability despite it’s abundance. This has been evidenced by China’s announcement in October 2021 that they will no longer be funding new coal projects abroad. The vulnerability of coal vs say natural gas is also evident in the EU’s discussions and debates around creating the Taxonomy for Sustainable Activities for the EU’s Green Deal i.e. the definitions applicable for then policy framework. One of the controversial elements of the Taxonomy is that gas and nuclear were to be included in part of green investment. The logic for inclusion is linked towards perceived practical necessity for gas to transition towards a net zero future. This is however versus the counter arguments which see doing so as a contradiction and therefore effectively green-washing as gas consumption should be actually on the decline in order to make net zero targets. The EU has delayed the decision on the Taxonomy elements to Northern Hemisphere autumn 2021 so this key decision is expected soon. Either way regardless of the final outcome, the opposing tensions in coming to the decision is the revealing aspect here and industrializing countries looking at gas for their energy needs will need to take note.

Another topic point bundled into this relates to whether renewables though cheaper and by in large emissions free, can majority facilitate the sort of growth required especially for low base industrializing countries. This also leads to questions around if they can provide base-load power given the issue of intermittency and that mass storage technology is still evolving. Some published work by IRENA and other similar works aim to show that the notion that renewables cannot provide base load power is a myth. However, from what it seems, though possible, the conditions under which this can be done require certain prevailing circumstances pertaining to inherent elements such as geography which determines the type of renewable access a country may have (e.g., access to geothermal or hydroelectricity) as well as the recurring theme of available funding to secure the infrastructure that can create such a system at scale.

2) Is ESG turning into a financial bubble?

The concept of Environmental, Social, and (Corporate) Governance or ESG based investing has come hand-in-hand with the narrative of the current times as a way for finance and funding to find a home residing in companies and activities that are perceived not to be harmful to the sustainability of the earth and people. In highly simplified terms, financial funds aiming to create these ESG funds will typically create them based on inclusion i.e. adding companies into fund based on how they score on ESG metrics or based on exclusion where one starts with a larger pool based on some predetermined basis e.g. the S&P500 then excludes companies that don’t meet or score favorably on selected ESG principles.

Given the topical nature of ESG, coupled with investor pressures as society progresses into churning investors who may want their money to be deployed “with a conscience”, there is an expectation that funding based on ESG principles will continue to grow. Indeed, the last few years have seen funding in ESG investment (see below) and related funds grow exponentially and an estimate believes that ESG assets under management will hit $53 trillion (almost 3 times the annual GDP of the US) by 2025 to constitute 1/3 of total global total assets under management.

However, concerns from some corners of financial industry have been raised as to whether the financial incentives arising from execution of ESG principles allign with and fulfill the goals set out to be achieved. This is given issues around data standardization and measurement as well potential disconnect on financial returns vs actual on-the-ground activities returns and also other factors such as funds having a premium participation fee. As a result, you may come across opinion editorials and interviews such as this one by a former Chief Investment Officer for Sustainable Investing where he expresses concern on ESG investing being a “dangerous placebo”.

Others will argue that is the way capital has always worked and the aspects that filter capital towards pushing innovation and rewarding industries that show worthiness in progressing mankind’s way of life are not easily separable from the industries that occupy the nebulous realm of not necessarily being in the public interest but simultaneously not being out-and-out illegal. Either way, this means we have to keep an eye on this complicated dynamic that intersects financial incentives, societal dynamics, and real-world outcomes when we engage with the results flowing out of the congress and beyond regarding how finances are mobilized in this era.

3) What direction will carbon market schemes take?

Given the complicated nature of driving reduction in carbon emissions from an incentive perspective due to the negative externality nature of the outcomes (i.e. the greenhouse effect of emissions not being isolable to the emitter), the commonly touted solution from an economics perspective is imposition of a carbon pricing mechanism. The aim of the mechanism would be to force internalization of the true cost of emissions by virtue of instituting a financial cost for emissions that forces the emitter to reduce their footprint otherwise risk economic survival especially when in the face of newer competition with lower footprints or contemporary competitors who manage to adapt. Currently there are about 64 regimes of carbon mechanisms and schemes globally covering approx 21% of total emissions as shown by the World Bank graphic below:

Some schools of thought such as that of the of World Trade Organization’s (WTO) Director General Ngozi Okonjo-Iweala believe in the adoption of a global price of carbon. This is believed to address challenges surrounding pricing inconsistency, standardization and measurement. This can then also act as a launchpad towards providing a methodical approach towards addressing emissions while also minimizing potential trade complications regarding measures like carbon border adjustments which will be part of the EU Green Deal. This Carbon Border Adjustment Mechanism (CBAM) will work as follows: “EU importers will buy carbon certificates corresponding to the carbon price that would have been paid, had the goods been produced under the EU's carbon pricing rules. Conversely, once a non-EU producer can show that they have already paid a price for the carbon used in the production of the imported goods in a third country, the corresponding cost can be fully deducted for the EU importer”. This means that beyond EU borders, exporters trading with the EU will implicitly have the dynamic of their level of low carbon/green production as a factor to manage in to their goods and therefore becoming factor affecting their level of competitiveness.

Another factor to consider around carbon pricing if we proxy it with other globally traded markets will be to what extent these markets – whether in the current fragmented form vs a unified form- will become an arena for speculative investment. This is a topical matter given hedge funds in the mix as well as the growth in easy access and cheap retail investing platforms that has characterized the current landscape at least from a narrative perspective. In this vain, the EU which has the world’s largest carbon market has had to consider moves to curb speculative investment after the significant growth in the emission permits in their cap-and trade scheme resulted in part from speculative investment by large scale investment groups and hedge funds. In a way, this could bear some analogies to the earlier point surrounding ESG and whether the mechanism drives desired outcomes or simply acts as an outlet for capital to do what capital does in the hands of society with different motivations and incentives. It could even be both with both elements conjoined into an amorphous package requiring constant steering and governance to yield desired results.

4) How do we manage the conflict between the science and the politics?

Each of these questions warrant their own articles, pieces and interviews so the idea is hopefully to continue bringing you key developments on the directions taken. The final question therefore doubles as a final thought as it in a way is an embedded theme across the previous questions already presented. This is a question regarding how we to manage the distinction between the politics and the science of agreeing and achieving the implied goals set out of improved livelihoods for all in a sustainable future. It would be naïve for us to believe that the process of consensus does not implicitly involve politics, so the issue becomes how are these balanced in order to get to the “truthful” solutions the world needs taking into account the different circumstances citizens, nations and corporations find themselves in across the world.

It is no secret that we generally live in a time where society feels more polarized around issues and we see that in the impasse-oriented public discourse (manufactured or real) and how aims at balanced views are seen as complicity or hypocrisy. The word “feels” here is emphasized again because we can see from history that the world has had many moments of extreme polarization on various issues and incidents. Therefore this sense of polarity is not unique to our moment but simultaneously does not negate acknowledging the nature of our moment. We can also observe that the Covid situation we are in has antagonized social structures through exposing inherent structural and under-rug-swept issues inevitably showing up in increased social unrest even in relatively peaceful countries.

It maybe that as humans, we are largely influenced towards only feeling the span of moment we preside over as opposed to say internalizing the sense behind polarity during a time we did not live through. This means having to push through using among many things, mental tools of empathy and also exposure to true historical context to engage and learn the lived experience of others. Another angle to the reason that this existential dread feeling potentially seems more intense probably also has to do with how some of the solutions that have come into being with reducing previous sources of conflict like globalization and technology have come with their own sets complications in new forms such as wider reaching echo chambers, so called fake news with the ability to permeate quicker and other social fabric related complexities. Given the social nature of our species, we therefore have an onus to actively figure out ways to improve society while simultaneously guarding against both a tyranny of the majority and at the same time an environment where extremes set the tone as those in the middle act as a silent buffer..