Electric Skies: Where are we in the journey to electrify aviation?

Are electric airplanes the future?

Flight has always been one of those phenomena that enamors the human imagination. We can see this exemplified in mythologies across global cultures that frequently associate flight with an aura of grandeur and even divinity. A modern-day extension of this even relates to concepts like TV & film superheroes where being able to seamlessly fly captures the essence of their powers. It is therefore no surprise that despite humans’ anatomical inability to fly, once the industrial revolution ushered in new energy sources and in turn improved manufacturing, mechanical flight became a reality in the early 20th century. Technology has since continuously improved to allow more people to experience this feat of human ingenuity – a feat which we may today take for granted but is no doubt a bookmark in the story of mankind.

With this background in mind and the knowledge of the overall discussion around the electrification of transport, mostly road vehicles, electrification of aviation is bound to enter the fray. It’s adjacency to vehicular electrification has meant increased discourse around what is in store for the aviation industry. Hence the goal of this piece is to summarize the latest developments and what they could mean for aviation’s future.

The Covid Pandemic Context

The aviation industry, particularly airlines, have the unenviable position of being amongst the hardest hit industries by the covid pandemic. These industries can be summarized in the acronym BEACH i.e., Bookings, Entertainment & Live Events, Airlines, Cruises & Casinos and Hotels & Resorts. The grim statistics as seen on the right, show projected 2021 airline passenger volumes that will be at approx. 50% of pre-pandemic levels (i.e. vs 2019) after the 2020 low of approx. 37%.

The International Air Travel Association, IATA, estimates that an optimistic view of air travel return to 2019 levels will be in 2023 with the pandemic having set passenger volumes back by about 2 years with respect to the growth outlook as shown below.

Where this demand destruction has been particularly threatening is in the business travel space given that these customers can typically make up 12 % of passenger volume but 75% of airline profit. While business travel is expected to make some sort of gradual recovery as currently being slowly seen in the US, it is debatable if previous peaks will be seen again anytime soon. This is predicated on that companies have a had a taste of far cheaper alternatives like online meeting and conferencing. This is particularly the case for companies in industries whose revenues regressed due to the pandemic but can be even for those that experienced growth. The incurrence of such lower costs while still delivering objectives may be difficult to fully reverse at a psychological level. The proverbial toothpaste cannot be put back into the tube - at least fully and neatly. The case for reduced business travel, and more so air travel overall, is further heightened when considering it at an international long-haul flight level where uncertainly of prevailing destination lockdown regulations, approved testing and clearance procedure still hampers ease and smoothness of travel.

The Case for Short Haul Flight

From on demand perspective, this prevailing environment favors servicing local flights particularly pertaining to leisure travelers. Local flying firstly has the advantage of having a lower scope for planning complications with respect to lockdown regulations and stranding changes. It also benefits from being an outlet for people to still engage in travel including to mentally decompress and see loved ones which the pandemic backdrop may have intensified as a desire. In addition to these demand factors, from an operational perspective, local travel-oriented airlines are more likely to have plane fleets that consist of a smaller variety of plane models meaning lower maintenance and equipment training costs among other things.

The relevance of this in the discussion on aviation electrification is that the impact of the pandemic can be seen to have emphasized the dynamics of short haul flying which is where the electrification journey of flying is beginning. This emphasis therefore forms a foundation so we can then look at the dynamics of the electrification of aviation given that the short haul presents the largest and most accessible opportunity for penetration.

Latest Developments in Electric Aviation

Hybrid Electric Planes

Much like the journey to electric vehicles where the initial big strides came through mixed technologies of fuel + batteries in a hybrid set-up, the electric aviation journey has been similar with early models focusing on hybrid technology . The first hybrid aircraft was the Diamond DA36 E-Star released in June 2011 developed by Siemens and Diamond. The plane was a two seater motor glider and the use of a hybrid system meant it used and produced 25% less fuel and emissions respectively.

Since then, other companies have developed varieties of hybrid aircraft .e.g. VoltAero with it’s 800 mile /1287km range Cassio hybrid aircraft it expects to have flying commercially by 2023. The 4-10 seater plane was first demonstrated in March 2020 and undertook a multi-stop demonstration tour in France in July 2021. According to the company’s CEO who is the former CTO at Airbus, the major advantage of the hybrid model is that use of fuel in the propulsion means that such planes can still have very competitive flight ranges compared to full electric aircraft which is analogous to the motor vehicle electric story. It is therefore not zero emissions though a sizeable step towards achieving it which is what the categories of electric aviation in sections below will discuss.

Another hybrid example is one developed by California based ZeroAvia which uses a hydrogen fuel cell and battery combination. There are still some challenges to overcome related to structural design to manage heat and overall challenges associated with hydrogen currently such as value chain development. However given the pace at which hydrogen is developing as an energy source this could change in the near future. The company is aiming for commercial development of the plane by 2023 with a targeted range of 500miles/ 804km

The Cessna Grand Caravan (eCaravan) by MagniX

May 2020 saw the demonstration flight for what is currently the world’s largest all electric plane– the Cessna Grand Caravan (or eCaravan) by Washington State, USA based company MagniX. The plane has a passenger capacity of 4 to 6 people and this flight took off from Grant County International Airport (about 182 miles/292km from Seattle) and was about 28 minutes in flight time. The design is based on the modification of the popular 13 passenger passenger or cargo “middle-mile” range plane (i.e. planes that typically cover 50-1000 miles/ 80-1609km), the Cessna 18 Caravan. The design still has to undergo further testing rounds to attain US Federal Aviation Authority (FAA) approval. Regardless of approval timelines, a lot can be learnt from details surrounding this maiden flight in terms of technology and limitations.

The flight used a 750 Volt Lithium-Ion battery weighting about 1 ton and requiring about 30 minutes of charging to complete the ~30-minute journey with a range of about 100miles/~160km climbing to a maximum altitude of 2500ft/762 meters. For a crude battery pack comparison, typical electric vehicle battery packs range from 400-800Volts . The energy cost of this flight subsequently worked out to about $6 of electricity as opposed to $300 equivalent kerosene cost. However, the equivalent weight of kerosene for this cost would fly the plane for a range of 1500miles/~ 2415km i.e. about 15 times further. These statistics reveal the overall challenge for electric air travel i.e. comparative energy density limitation in turn limiting flight range. However, MagniX believes the 1000 mile/~1610km maximum flight range segment is a viable target for disruption as technological improvements continue. This range currently makes up about half of passenger flight volumes so indeed presents an exciting prospect.

Electric vertical-takeoff-and-landing vehicles (eVTOLs)

Another approach to short range aviation can be seen through the concept of Electric Vertical-Takeoff-and-Landing vehicles, or eVTOLs (pronounced ee-vee-tols). These can be seen in some way as a form of electric helicopter given that helicopters are themselves VTOLs though designs of eVTOLs show deviation given different propulsion structures even among different eVTOL manufacturers.

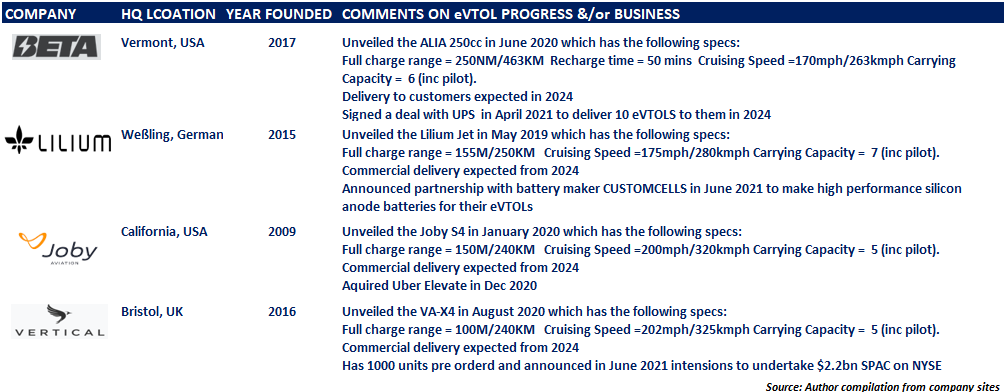

The idea of eVTOLs has also gathered momentum because of the advent of ride hailing companies such as Uber who have been strategizing how to take ride hailing to the skies in the form of air-taxis. In December 2020, Uber itself announced the sale of their air-taxi development division called Uber Elevate (previously called UberCopter) to Joby Aviation and despite this sale, Uber and Joby will continue cross application partnership. Joby is one of the startups working in this space as summarized below. .

Other companies in the mix include California based Archer Aviation and Guangzhou, China based eHang. The traditional big players known for aviation equipment such as Boeing and Airbus are also involved. Despite Boeing discontinuing their 2 year old urban mobility NeXt program as a result of the negative impact of 737 Max troubles as well as covid related downturn, they are backing another California based eVTOL startup, called Wisk Aero. Airbus has developed its own eVTOLs including the autonomous 4 passenger carrying CityAirbus which had a short demonstration shown on the 29th of July 2021 . Airbus also has the single passenger carrying Vahana. Ideally from a set up perspective, all these eVTOLs would typically use what is termed as “vertiports” as their takeoff and landing infrastructure which would be similar to typical helipad set up but with additional structures such as charging at the most comparable level.

While the market path of eVTOLs is new and emerging , a December 2018 report by Morgan Stanley puts a base case of the eVTOL market at $1.5 trillion by 2040 which is comparable the annual GDP of a country like Australia or Brazil today.

Incidentally, progress in this space can also be seen to be analogous to the area of drones which can have a look similar to eVTOLS but don’t necessarily require the same infrastructure. This is due to lower size requirements by and large and having the key distinction of being unmanned which also reduces safety and weight complexity. As battery, imaging and overall remote technology improves, drone technology’s array of benefits continue to spread and facilitate many areas such as goods delivery (e.g., food, health products), surveillance (e.g., police, nature conservation, farming), equipment inspection (e.g., electric pylons), weather forecasting and many similar fashions of use.

Final Thoughts

As we hurtle towards some of the advancements mentioned here, there is a large reliance on progress in key areas particularly hybrid technology, battery technology and regulation. Battery technology advancement will be needed to keep planes sufficiently light but with enough energy density to allow flight ranges to increase and therefore boost scope. This includes possibilities like using Solid State batteries, Lithium Sulfur batteries or alternatively going the hydrogen fuel cell route. Given the importance of battery and fuel cell technology variables to developments in the electromobility space, they call for separate coverage in future articles.

We know it will be a while until we see the sort of ranges we see in kerosene/jet fuel based planes which allow for high volume long haul travel but as established, this does not negate the possibility of disruption in the short haul arena. Regulation is another area of challenge where certification of designs still proves to be a hurdle. This is due to the new configurations and propulsion structures applied in the variety of electric aviation vehicles being developed which are in essence being learnt in real time from a regulatory perspective. However this regulatory challenge might not be as bad as it sounds viewed from another perspective because to a degree, regulatory tension is a direct by-product of innovation. So one could say as a society we are not fully innovating if regulatory change does not become warranted.